Corporate America has capped off an outstanding 2021 with an excellent fourth quarter earnings season so far. Entering 2021, the consensus estimate for S&P 500 Index earnings per share (EPS) was less than $170. Now with fourth quarter results mostly in the books, that number is 22% higher at $208. Here we recap another solid fourth quarter earnings season and discuss what the results could mean for earnings growth and stock market performance in 2022.

Delayed Investor Shift From Macro to Micro

In our earnings preview on January 10, we noted that we welcomed a shift from the macro to the micro. Well, given the path of inflation, the resulting dramatic shift in Federal Reserve (Fed) rate hike expectations, and the escalating Russia-Ukraine conflict, that shift hasn’t really happened. However, when we turn our attention away from macro headlines to corporate America, we find that companies have again showcased their ability to effectively manage through the pandemic’s challenges, notably supply chain disruptions and labor and materials shortages that have pushed costs higher.

Great Numbers

The numbers this earnings season have been great even without considering that the bar has been raised consistently throughout the pandemic. S&P 500 earnings per share are tracking to a 31% year-over-year increase, shown in [Figure 1], roughly 10 percentage points above the consensus estimate when earnings season began. That upside will likely fall a bit short of the 12 points of upside in the third quarter, but considering the long-term average upside is about five percentage points, and the fourth quarter was wrought with pandemic-related challenges, we’re quite impressed. In fact, in our earnings preview last month, we wrote, “Earnings growth approaching 30%, though slower than the third quarter’s near-40% clip, would be impressive given the challenging operating environment.”

How Have They Done It?

Though about 75 S&P 500 companies have yet to report, companies have generally beaten estimates soundly again with a combination of surprising revenue strength and resilient profit margins. Fourth quarter 2021 revenue came in about three percentage points above consensus estimates at more than 15.5%, bolstered by the strong economic growth in the quarter (6.9% real gross domestic product growth annualized), fueled by inventory restocking, as well as price increases. That 15.5% revenue growth is higher than any quarter during the previous economic expansion (2009-2020), but was bested by the second and third quarters of 2021 that saw growth inflated by base effects coming off 2020 lockdowns.

This solid revenue upside, which is about twice the long-term average “beat”, came despite supply chain disruptions limiting what companies had available on the shelves to sell, labor shortages that cost companies sales they otherwise would have booked, and the COVID-19 Omicron wave in late November through December that constrained economic activity.

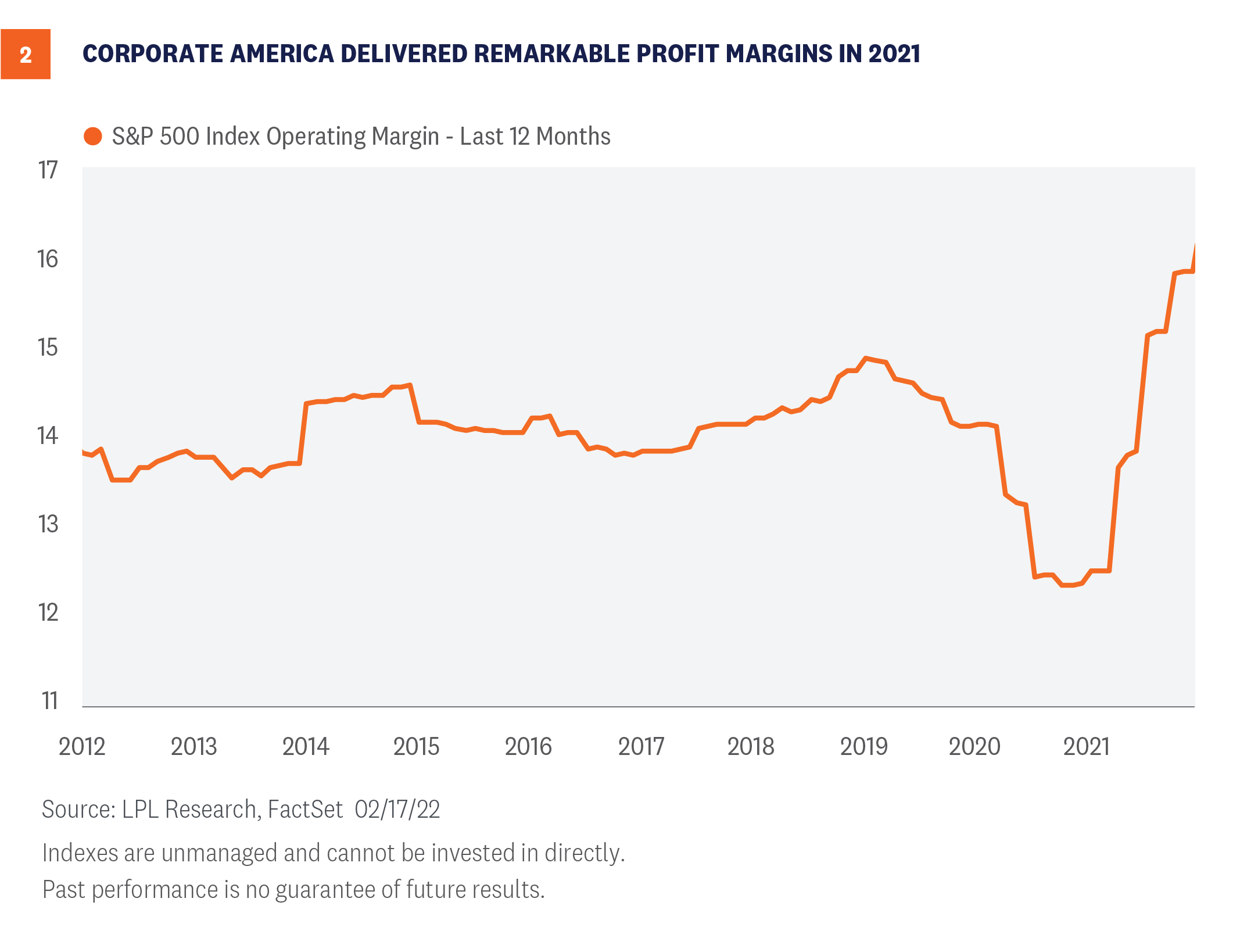

The other part of the earnings story is the impressive profit margins. Due to rising costs of labor, materials, energy, and transportation, we had anticipated some meaningful profit margin compression in the quarter. It looks like we’ll end up with a slight downtick in margins quarter over quarter when all the results are in, but it won’t be as big of a drop as we had feared.

That slight potential dip from the third quarter to the fourth doesn’t take away from the fact that margins last year were tremendous [Figure 2]. Companies are enjoying pricing power, which is helping them pass along higher costs, notably wages, and largely preserve those high margins that are well above pre-pandemic levels.

Carrying Earnings Momentum Into 2022

We remain concerned about higher wages and other inflation pressures crimping margins in 2022. Supply chain challenges will likely linger through the first half of the year based on commentary from a number of companies in recent weeks. Still, the impressive profitability displayed in the fourth quarter puts corporate America in a strong position to potentially deliver higher earnings in 2022 than we previously anticipated.

On the revenue side, remember higher prices translate into more sales, as long as demand remains strong enough to pay those higher prices. Pricing power helped companies in the fourth quarter and should continue to help in 2022. If the U.S. economy grows near our 4% forecast in real terms this year, adjusted for inflation, and consumer inflation adds another five points (consensus forecast of economists according to Bloomberg), then we believe 9% revenue growth from S&P 500 companies is a reasonable expectation. For perspective, the best revenue growth years since the 2008-2009 financial crisis were 2011 (+12.5%) and 2021 (+16.9%).

That means our 6-7% earnings growth forecast for 2022 could be attainable even with modest margin compression (with some help from share repurchases reducing the denominator in the earnings-per-share calculation). For now, we’ll maintain our forecast of $220 in S&P 500 EPS in 2022, but that number could be too low based on the earnings momentum evident this earnings season. The consensus estimate for 2022 S&P 500 EPS rose 0.5% during earnings season, much better than the average 2-3% reduction observed historically.

Macro Backdrop Still Supports 5,000 on the S&P 500 at Year End

Stocks have gotten off to a rough start this year. The adjustments to higher inflation and more Fed rate hikes have been difficult, while the Russia-Ukraine situation has added to market anxiety and volatility. While it may take more time for the market to shift its focus toward solid company fundamentals and get more comfortable with the inflation outlook, we expect stocks to recover early-year losses and rally back to new highs through year-end as that transition takes place.

Mid-cycle years such as 2022 tend to see double-digit gains for stocks, even more optimistic than the high-single-digit gain we forecasted in our Outlook 2022: Passing the Baton. History shows that stocks tend to do well during the year after initial Fed rate hikes and that volatility related to geopolitical events has frequently been short-lived. The additional reopening of the economy that lies ahead makes solid growth in the U.S. economy and corporate profits, in our opinion, more likely this year and should help ease inflation pressures, solidifying a favorable backdrop for attractive stock market returns in 2022.

The recent move higher in interest rates doesn’t change the calculus much for us in terms of stocks versus bonds. We continue to recommend an overweight allocation to equities and an underweight fixed income allocation relative to investors’ targets, as appropriate.

______________________________________________________________________________________________

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

U.S. Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio.

Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability. Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio.

All index data from FactSet.

This research material has been prepared by LPL Financial LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

| Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Guaranteed | Not Bank/Credit Union Deposits or Obligations | May Lose Value |

RES-1056300-0222 | For Public Use | Tracking # 1-05246331 (Exp. 2/23)